Polysilicon Ingot Market Valued at USD 9.45 Billion in 2024, Projected to Reach USD 18.73 Billion by 2032

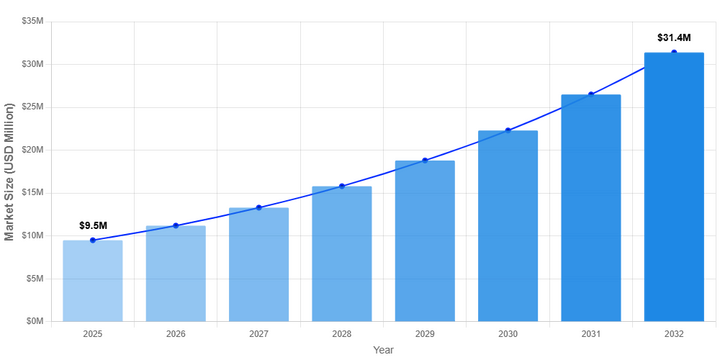

Global polysilicon ingot market size was valued at USD 9.45 billion in 2024. The market is projected to grow from USD 10.12 billion in 2025 to USD 18.73 billion by 2032, exhibiting a CAGR of 8.2% during the forecast period. Polysilicon ingots are high-purity silicon materials produced through the Siemens process or fluidized bed reactor method, serving as the foundation for photovoltaic cells and semiconductor devices.

These crystalline structures, categorized by purity levels from 6N (99.9999%) to 11N (99.999999999%), are critical for solar and semiconductor manufacturing. The market growth is fueled by the rapid adoption of solar energy and rising semiconductor demand driven by AI and 5G technologies. While China dominates global production with over 85% share, regional diversification is accelerating. Key players like Wacker Chemie and GCL Tech are investing in granular silicon technologies that reduce energy consumption by up to 40% compared to conventional processes. The 11N purity segment is projected to register a strong 12.1% CAGR through 2032.

Get FREE Sample Reports:https://www.24chemicalresearch.com/download-sample/207730/global-polysilicon-ignot-forecast-market

Market Drivers

Growing Solar Energy Adoption to Fuel Polysilicon Demand

Global renewable energy transitions are significantly increasing polysilicon demand. Solar installations reached approximately 270 GW in 2023, with continued double-digit growth expected through 2032. Government incentives such as the U.S. Inflation Reduction Act and EU renewable initiatives are supporting localized polysilicon production and reducing fossil fuel dependency.

Semiconductor Industry Evolution Creating New Demand Channels

The semiconductor sector represents a fast-growing opportunity for polysilicon producers. Expanding 5G, IoT, and AI chip manufacturing is driving demand for 9N–11N purity silicon. Semiconductor-grade polysilicon consumption rose 12% in 2023, as chipmakers increase production capacities to address global supply constraints.

Vertical Integration Strategies Enhancing Market Stability

Leading solar panel manufacturers are pursuing vertical integration, securing ingot supplies to ensure consistent material quality and reduce price volatility. Over 60% of new capacity announcements in 2024 included backward integration into ingot production, strengthening the industry’s long-term stability.

Get FREE Sample Reports:https://www.24chemicalresearch.com/download-sample/207730/global-polysilicon-ignot-forecast-market

Market Restraints

Energy-Intensive Production Processes

The Siemens process consumes 60–80 kWh per kilogram of polysilicon, posing significant energy cost challenges. Although fluidized bed reactor technologies can cut energy use by up to 40%, adoption remains limited due to high setup costs.

Geopolitical Tensions and Supply Chain Disruptions

Trade restrictions and logistics issues have caused price fluctuations exceeding 50% within single quarters. Semiconductor-grade polysilicon is particularly affected, as few suppliers can meet its stringent quality standards.

Technological Substitution Risks

Emerging alternatives such as thin-film and perovskite solar technologies could impact traditional polysilicon demand. While polysilicon will remain dominant through 2032, producers must continue investing in efficiency and cost reduction.

Get FREE Sample Reports:https://www.24chemicalresearch.com/download-sample/207730/global-polysilicon-ignot-forecast-market

Market Opportunities

Emerging Markets Offer Untapped Growth Potential

Rapid solar adoption in Southeast Asia, Africa, and Latin America is creating new opportunities. India’s Production Linked Incentive (PLI) scheme and other national initiatives are enabling domestic manufacturing capabilities.

Niche Applications Driving Premium Product Demand

Ultra-high-purity (11N+) silicon for quantum computing and aerospace applications commands prices 5–7 times higher than standard grades. These specialized applications offer significant margin expansion opportunities for producers investing in tailored manufacturing.

Market Trends

Expanding Solar Energy Demand

The global shift to renewable energy continues to drive polysilicon ingot market growth. Nations are investing heavily in solar manufacturing capacity to reduce import dependency, reinforcing polysilicon’s central role in PV systems.

Semiconductor Sector Expansion

High-purity polysilicon remains essential for the next generation of microelectronics and chips. Innovations in AI processors and nanometer-scale chip design are increasing global demand for ultra-pure silicon wafers.

Technological Advancements in Manufacturing

Upgrades in Czochralski (CZ) and Directional Solidification (DS) methods, alongside AI-driven quality control, are improving production yields and energy efficiency.

Regional Supply Chain Diversification

Geopolitical shifts are accelerating regional polysilicon production in North America and Europe, reducing reliance on Asian suppliers while strengthening local energy security.

Get Full reports Here:https://www.24chemicalresearch.com/reports/207730/global-polysilicon-ignot-forecast-market

Competitive Landscape

The global market remains semi-consolidated, with major players focusing on technological innovation and capacity expansion.

Leading Companies:

• GCL Tech (China)

• Wacker Chemie AG (Germany)

• Hemlock Semiconductor (U.S.)

• Daqo New Energy (China)

• OCI Company (South Korea)

• REC Silicon (Norway)

Want To Lead The Chemical Market? Discover How Today

https://www.linkedin.com/pulse/high-silicon-cast-iron-anodes-industry-valued-iawae

https://www.linkedin.com/pulse/macrocyclic-musk-industry-valued-usd-257-million-sul8e

Key Developments:

- GCL Tech leads with 120,000 MT annual capacity and full solar value chain integration.

- Wacker Chemie AG and Hemlock Semiconductor collectively hold 35% share of the high-purity segment.

- Daqo New Energy commissioned a 100,000 MT facility in Xinjiang to meet PERC and TOPCon solar demand.

- OCI Company leverages recycling technologies that cut production costs by up to 15%.

Get Full reports Here:https://www.24chemicalresearch.com/reports/207730/global-polysilicon-ignot-forecast-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch delivers advanced chemical market intelligence to over 30 Fortune 500 clients. We provide actionable insights through:

• Plant-level capacity tracking

• Real-time price monitoring

• Techno-economic feasibility studies

With a decade of specialized expertise, our team delivers data-driven reports that support strategic business decisions in the global chemicals and materials sectors.

International: +1 (332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch