Global Glass Core Substrates Market to Reach USD 572 Million by 2034 Powered by AI Chip Packaging

Posted by shraddha thakur

Filed in Technology 333 views

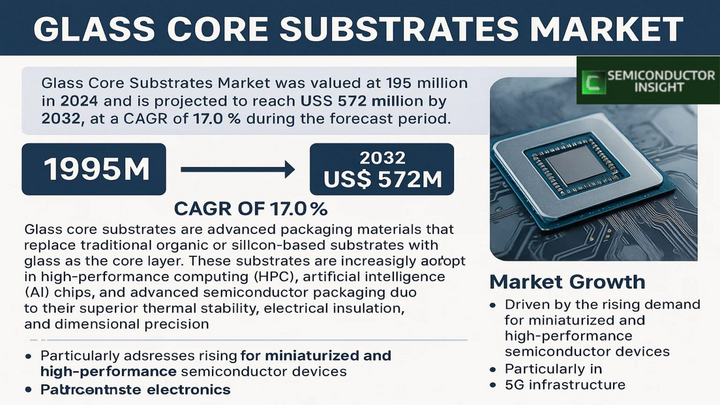

Global Glass Core Substrates Market was valued at USD 195 million in 2026 and is projected to reach USD 572 million by 2034, exhibiting a CAGR of 17.0% during the forecast period 2026-2034. This rapid trajectory reflects surging adoption in high-density interconnects for next-gen processors.

Glass core substrates utilize inorganic glass panels as the structural base in advanced semiconductor packages, replacing organic laminates or silicon interposers to enable finer pitches below 2μm, CTE matching silicon (3-5 ppm/°C), and dielectric constants under 4.0 for mmWave signals. Fabricated via laser via drilling, metallization, and TGV (through-glass via) formation, they support 3D stacking in chiplet designs and co-packaged optics. Deployed in HPC GPUs, AI accelerators, 5G RF modules, and EV powertrains, glass enables 50% lower warpage versus epoxy and supports panel-level scaling to Gen3 (510x515mm).

👉 Access the complete industry analysis and demand forecasts here: https://semiconductorinsight.com/report/glass-core-substrates-market/

Market Definition and Dynamics

Glass core substrates represent the interposer layer in 2.5D/3D packaging, bridging dies with ultra-fine RDL (redistribution layers) at 1/1μm L/S. Macro forces include AI training clusters demanding 10x I/O density and PLP cost reductions targeting 30% below silicon bridges. With WLP claiming 60% applications, dynamics center on yield ramps above 90% for TGV fills and ecosystem standardization via SEMI-G14.

Asia-Pacific's 80% dominance stems from OSAT capacity in Taiwan/China, with NA/EU at 16%/3%.

Market Drivers

- Explosive HPC/AI chip demand requiring low-loss substrates for 100+ Gbps SerDes links.

- WLP/PLP transitions enabling 20-30% cost-per-wafer savings at Gen3 scales.

- 5G/IoT RF front-ends needing Dk<3.5 glass for sub-6/mmWave modules.

- Automotive ADAS/EV traction inverters mandating 200°C thermal stability.

Market Restraints

- 30-40% cost premium over organic substrates delaying mainstream adoption.

- TGV laser drilling yields below 85% for >100k vias/panel.

- Brittle fracture risks during dicing/handling without edge strengthening.

Market Opportunities

- Chiplet ecosystems for AMD/Intel next-gen CPUs with glass bridges.

- Co-packaged silicon photonics integrating lasers on glass cores.

- European/North American fab reshoring via CHIPS Act subsidies.

Competitive Landscape

Japanese glass majors command 90% share through precision melting and polishing at <10nm flatness. AGC/Schott lead with low-CTE borosilicates; Corning advances fusion-drawn panels. Competition intensifies on via density (>500/μm² and panel warpage control.

and panel warpage control.

Capacity expansions target 50k m²/year by 2028 for PLP qualification.

List of Key Glass Core Substrate Companies

- AGC Inc.

- Schott AG

- Corning Incorporated

- Hoya Corporation

- Ohara Corporation

- Dai Nippon Printing Co., Ltd.

- Nippon Electric Glass (NEG)

- CrysTop Glass

- WGTech

Segment Analysis By Type

- CTE Above 5 ppm/°C: 65% share; optimal silicon matching prevents die cracking in stacks.

- CTE Below 5 ppm/°C: Niche for RF; ultra-low loss at 77GHz automotive radar.

By Application

- Wafer Level Packaging: 60% volume; HBM4 integration for Nvidia/AMD GPUs.

- Panel Level Packaging: 25% CAGR; Gen3 panels cut costs 25% for volume AI chips.

Regional Insights

Asia-Pacific rules at 80% with TSMC/Samsung PLP pilots; North America grows 25% CAGR via Intel's glass interposer for Lunar Lake; Europe leverages Schott for auto radar modules; emerging regions lag due to packaging immaturity.

👉 Access the complete industry analysis and demand forecasts here:

https://semiconductorinsight.com/report/glass-core-substrates-market/

📄 Download a free sample to explore segment dynamics and competitive positioning:

https://semiconductorinsight.com/download-sample-report/?product_id=117945

About Semiconductor Insight

Semiconductor Insight is a global intelligence platform delivering data-driven market insights, technology analysis, and competitive intelligence across the semiconductor and advanced electronics ecosystem. Our reports support OEMs, investors, policymakers, and industry leaders in identifying high-growth markets and strategic opportunities shaping the future of electronics.

🌐 https://semiconductorinsight.com

🔗 LinkedIn:Follow Us

📞 International Support: +91 8087 99 2013